Funded trading accounts give traders access to capital they could never afford personally, in exchange for a share of the profits. You pay an evaluation fee, prove you can manage risk, and the prop firm hands you an account ranging from $10,000 to $400,000 to trade with.

Key Takeaways

- A funded trading account gives you access to firm capital after passing an evaluation, with profit splits typically ranging from 70% to 90%.

- The evaluation costs $50-$1,000 depending on account size, takes 10-30 days, and tests your ability to trade profitably within strict risk parameters.

- Realistic monthly earnings on a $50,000 funded account are $1,000-$2,500 for consistently profitable traders.

- Most funded traders blow their first account within 6 weeks due to psychological pressure, not lack of skill.

- Funded accounts work best for traders with proven skills but limited personal capital.

On This Page

- What Is a Funded Trading Account?

- How Funded Accounts Actually Work

- How to Get a Funded Account

- What Happens After You Get Funded

- Funded Account Types

- How Much Funded Traders Make

- The Rules That Govern Funded Accounts

- Funded vs Personal Account

- How Traders Get Paid

- Common Mistakes That End Funded Accounts

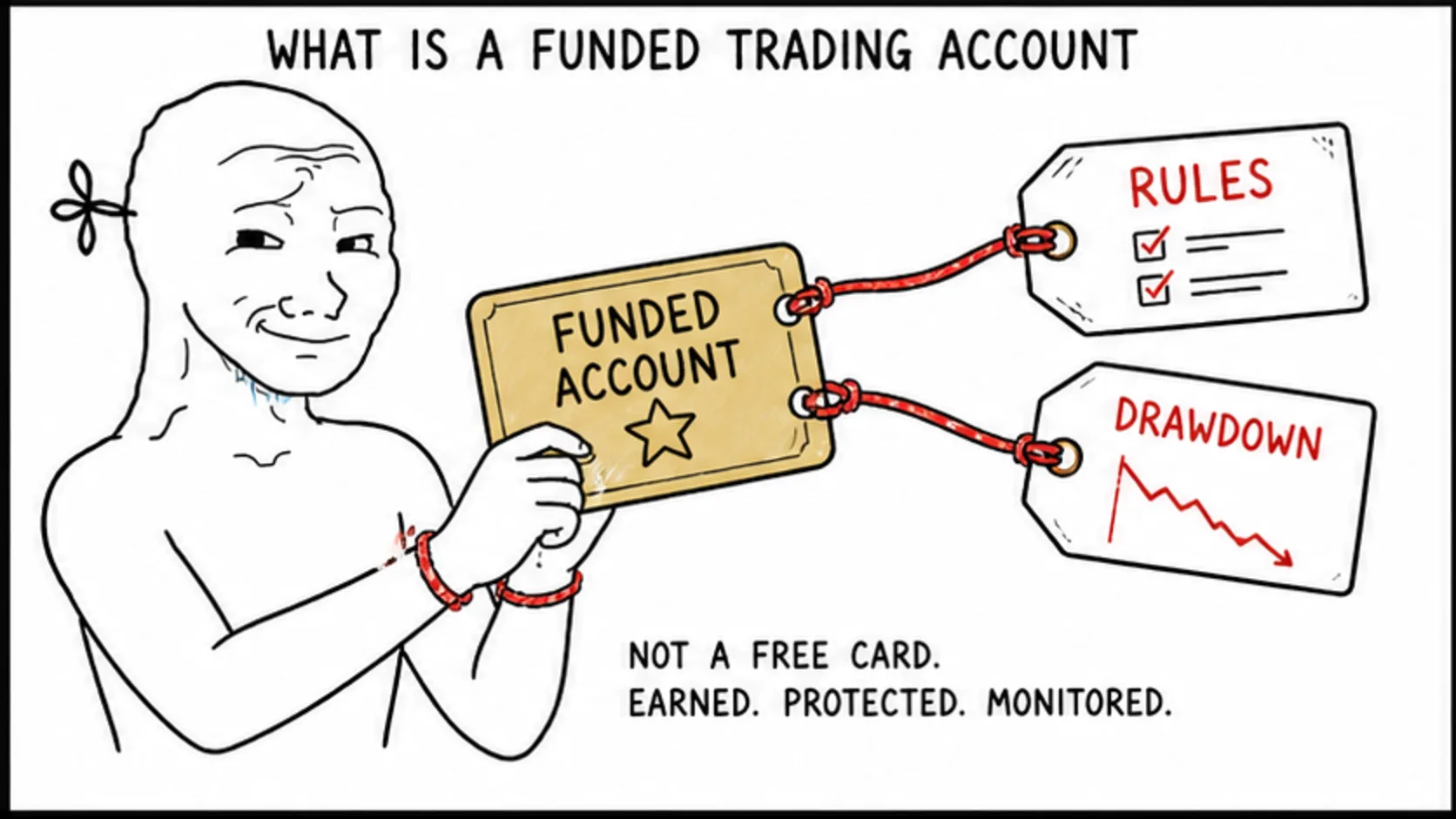

What Is a Funded Trading Account?

A funded trading account is exactly what it sounds like. An account funded by someone else's money that you get to trade after proving yourself through an evaluation.

Here's the basic math. You pay a $200 evaluation fee for a $50,000 account. You pass the evaluation by hitting a profit target while staying inside the firm's risk rules. Once funded, you keep trading and taking home 80% of whatever you earn.

Make $2,000 in a month on a funded account, you get $1,600. The firm keeps $400. That's the entire deal, and when you frame it that way, it's a remarkably fair arrangement for access to $50,000 in capital you didn't have to deposit.

This is different from a personal trading account where you deposit your own money and keep 100% of profits. A funded account trades firm capital, follows firm rules, and splits profits.

Most funded accounts trade on simulated servers that mirror live market conditions. Your trades execute against real prices with real spreads. The experience is functionally identical to live trading.

Think of the funded account as a job interview that never ends. You proved you could trade during the evaluation. Now you have to keep proving it every single day, with rules watching your every move.

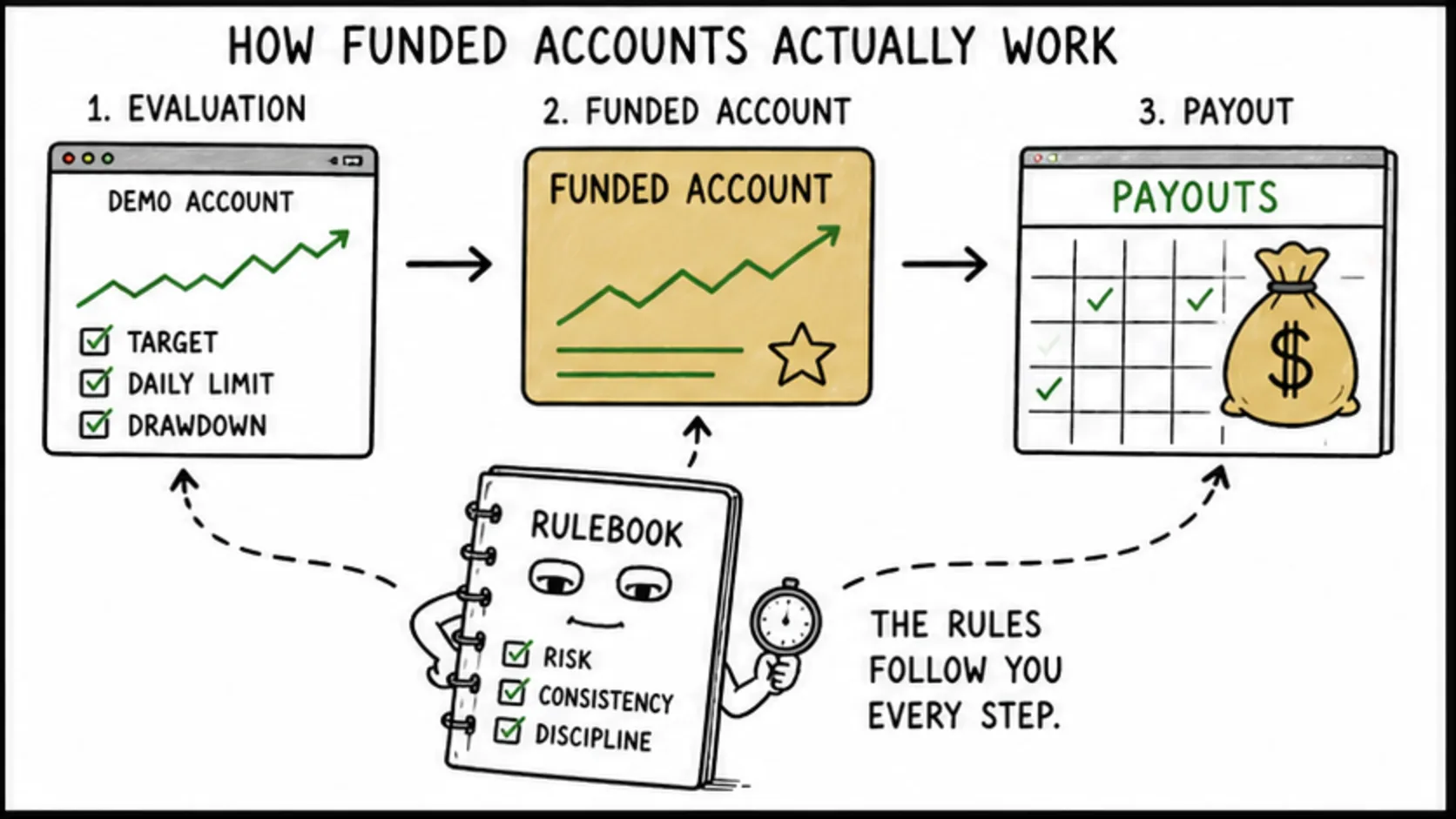

How Funded Accounts Actually Work: The Full Process

The lifecycle of a funded account has two distinct phases: the evaluation and the funded phase. Understanding both before you start is what separates prepared traders from people who donate fees to prop firms.

Phase one is the evaluation. You select an account size, pay the fee, and receive login credentials. You trade the account according to the firm's rules, trying to hit a profit target within a time limit.

Most firms set the target at 8-10% of the account balance, with a time limit of 30-60 calendar days and strict drawdown rules. The evaluation rules are deliberately restrictive, testing whether you can generate profits while managing risk.

Phase two is the funded account itself. You passed the evaluation, received your funded credentials, and now you're trading with real consequences. The rules are typically slightly relaxed compared to the evaluation.

The transition between phases catches people off guard. During the evaluation, your only job is hitting a target. During funded trading, your job is being consistently profitable month after month while following rules that will close your account if you slip up.

How to Get a Funded Trading Account: Your Step-by-Step Path

Getting funded follows a clear sequence. But most beginners skip steps and wonder why they keep failing evaluations.

Step one: learn to trade. Not "watch a few YouTube videos and think you understand price action." Actually learn. Practice on a free demo account for at least a month. Develop one strategy you can execute without hesitation. See the full approval process broken down step by step.

Step two: choose a prop firm. Our head-to-head comparison of every major prop firm breaks down the rules, costs, and payout records of the top firms. Research firms based on their rules, payout history, and reputation, not their marketing. The firm with the flashiest website isn't always the best choice.

Step three: pick your account size carefully. Start with $10,000 or $25,000, not $200,000. The difficulty doesn't scale linearly with account size, but the psychological pressure certainly does.

Step four: execute the evaluation. One trade at a time, one day at a time. Don't rush. The time limit matters less than protecting your account. A slow pass is still a pass. A fast fail is still a fail.

Step five: receive your funded account credentials. Congratulations, now the real work begins. Set up your risk parameters, establish your daily routine, and treat the funded account with the same discipline you showed during the evaluation.

What Happens After You Get Funded

This is the part most guides skip, and it's where most funded traders run into trouble. The celebration of passing your evaluation lasts about a day.

The first week of funded trading is critical. Every emotion you suppressed during the evaluation comes flooding back. You're no longer chasing a target, you're trying to build consistency.

Payouts work on a schedule. Most firms pay every 14-30 days after your first profitable period. Some firms offer on-demand payouts after an initial probation period.

Scaling is the long-term benefit nobody talks about enough. A trader who maintains profitability over 3-6 months can see their account grow from $50,000 to $100,000 to $200,000 and beyond, without paying additional evaluation fees.

The statistics are sobering though. Industry conversations suggest the majority of funded traders lose their first funded account within the first two months. Not because they can't trade, but because they trade differently when real payouts are on the line.

Funded Account Types: Forex, Futures, Crypto and More

The type of funded account you choose determines what you trade, which platform you use, and what rules apply. The two dominant categories are forex and futures.

Forex funded accounts are the most common type available. You trade currency pairs on MetaTrader 4, MetaTrader 5, or cTrader. The daily forex market volume is roughly $7.5 trillion according to the Bank for International Settlements, making it the deepest market for prop firm trading.

Futures funded accounts trade contracts on indices, commodities, and interest rates. The most popular instruments are E-mini S&P 500 (ES), E-mini Nasdaq (NQ), crude oil (CL), and gold (GC). Futures accounts tend to have lower evaluation fees but steeper learning curves.

Crypto funded accounts are newer and carry additional risk. The volatility is extreme, markets run 24/7, and the rules tend to be stricter around position sizing and drawdown limits.

Beyond instrument type, there are also different funding structures. Challenge-based accounts require passing an evaluation first. Instant funding accounts skip the evaluation but charge higher fees with stricter rules.

How Much Do Funded Traders Actually Make?

Let's do the math, because the marketing materials won't. Your earnings depend on three things: account size, your profitability percentage, and the profit split.

On a $50,000 account, a trader making 3% per month generates $1,500 in profit. With an 80% profit split, you take home $1,200 per month. Solid, consistent, but not life-changing from a single account.

On a $100,000 account at 5% monthly profit with an 80% split, you're earning $4,000 per month. That's $48,000 per year from prop trading. But 5% monthly is exceptional consistency, not the norm.

The $50K vs $200K comparison is important. A $200,000 account doesn't mean four times the profit. It means bigger position sizes, higher dollar-value risk per trade, and significantly more psychological pressure.

The honest range for most funded traders is $500-$3,000 per month. Exceptional traders earn $5,000+. The traders making $10,000+ monthly are running multiple funded accounts simultaneously.

The Rules That Govern Funded Accounts

Funded accounts are not the wild west. Every firm enforces rules that can close your account instantly if violated. Understanding these rules is more important than understanding any trading strategy.

The daily loss limit is the most commonly breached rule. It caps your daily loss at 4-5% of the account balance. On a $50,000 account, that's $2,000-$2,500. Sounds like a lot until you have three consecutive losing trades and decide to "make it back" with one oversized position.

The maximum drawdown is your total leash. Typically 10-12% of the starting balance. On that same $50,000 account, you can lose $5,000-$6,000 total before the account closes.

Trading restrictions vary by firm. Common ones include no trading during high-impact news events, no holding positions over weekends, no hedging, and no copy trading between accounts.

The consistency rule states that no single trading day can account for more than 30-40% of your total profits. This prevents traders from getting lucky on one trade and passing while being inconsistent across the board.

Funded Account vs Personal Account: Which Is Right for You?

This debate runs through every trading community on Reddit. The answer depends entirely on your situation.

Funded account advantages: access to $50,000-$400,000 in capital you probably don't have personally. Your maximum financial loss is the evaluation fee. You get forced discipline from firm rules. And profit splits of 70-90% are genuinely generous when you're risking none of the capital.

Funded account disadvantages: you give up 10-30% of profits forever. You must follow someone else's rules. Your account can be closed for rule violations regardless of profitability. And the evaluation process costs money with no guarantee of passing.

Personal account advantages: you keep 100% of profits. No rules beyond what your broker enforces. Complete freedom over trading style, position sizing, and schedule. No one can close your account.

Personal account disadvantages: limited by your own capital. $5,000 in a personal account is $5,000 of actual money at risk. No forced risk management. And the emotional weight of losing your own money is significantly heavier than losing firm capital.

Here's the bottom line. Funded accounts are best for traders who have demonstrable skill but limited capital. If you have $100,000 in a brokerage account, you probably don't need a prop firm. If you have $2,000 and can trade consistently, a funded account makes sense.

How Traders Get Paid: Payouts Explained

The payout process is simpler than most traders expect, but there are nuances worth knowing.

Most firms require a minimum profit threshold before your first payout, usually $100-$500. After that first payout, subsequent withdrawals are processed every 14-30 days or on-demand for premium account types.

The payout request process is straightforward. You submit a withdrawal request through the firm's dashboard. The firm reviews your trading activity to confirm no rule violations occurred.

Payment methods vary by firm. Bank transfers, cryptocurrency (usually USDT or BTC), and e-wallets like Deel are the most common options. The profit split is applied before the payout reaches you. Our full guide to prop firm payouts covers every method, timeline, and red flag.

Denied payouts are the biggest fear for funded traders. Legitimate reasons include rule violations detected during review. Questionable reasons include vague "strategy inconsistency" flags that weren't clearly defined in the terms.

Understanding why payouts get denied before you start trading is essential. Read the terms, follow the rules, and document everything.

Common Mistakes That End Funded Accounts

You'd think getting funded would be the hard part. For most traders, keeping the account is harder. Here are the mistakes that end funded accounts.

Mistake one: sizing up immediately after getting funded. You passed the evaluation trading 0.5 lots. Now you're funded and trading 2.0 lots because "it's not my money." It's not your money, but it is your funded account, and overleveraging will close it just as fast.

Mistake two: abandoning your strategy because the target is gone. During the evaluation, you had a clear plan. Now you're funded and experimenting with new setups mid-session. Stick with what got you here.

Mistake three: revenge trading after a drawdown day. Your daily loss limit is sitting there, watching you, waiting for you to make one stupid decision. That oversized revenge trade is the one that ends your funded account.

Mistake four: not tracking your drawdown in real time. Use a drawdown calculator to know exactly where you stand relative to your limits at all times. Traders who don't track drawdown are the ones who breach it by $50 and lose a $50,000 account over a rounding error.

Most people don't lose funded accounts because they can't trade. They lose them because they trade fine for 20 days and then blow it all on one terrible session. Learning how not to self-destruct is more valuable than any strategy you'll ever learn.

Whether you're ready for a funded trading account or still building your skills, the path from beginner to consistently funded trader is the same. Learn the rules, manage the risk, and stop making the same expensive mistakes. The funded traders aren't smarter than you. They just stopped self-destructing long enough to let their edge work.