Prop trading firm regulation news in 2026 is dominated by one theme: regulators are catching up to an industry that grew faster than anyone expected. The Financial Conduct Authority, the Commodity Futures Trading Commission, and the European Securities and Markets Authority have all taken actions that directly affect how prop firms operate, how they pay traders, and whether they can continue offering services in certain jurisdictions.

Here is what is actually happening, what it means for your funded account, and what to watch for next. No spin, no panic, just the facts.

Key Takeaways

- Prop firm regulation is tightening globally, with the FCA, CFTC, and ESMA all increasing scrutiny of retail prop trading firms in 2025-2026.

- The key regulatory concern is that some prop firms operate like unlicensed brokers, which regulators view as a risk to retail traders.

- KYC and AML requirements are becoming standard across the industry, even for firms that were previously unregulated.

- Regulation is not the end of prop trading. Properly structured firms are adapting and will survive the crackdown.

- As a trader, you should verify your firm's compliance status and avoid firms that resist basic regulatory requirements.

On This Page

Why Regulators Are Paying Attention Now

The prop firm industry went from niche to mainstream in about three years. During that growth spurt, most retail prop firms operated in a regulatory grey zone. They were not brokers, because traders never deposited their own capital. They were not investment advisors, because they did not tell you what to trade. They were something new, and regulators had not caught up.

That changed when the industry hit an estimated $8 billion in annual evaluation fee revenue. Suddenly regulators noticed that millions of retail traders were sending money to offshore entities with minimal oversight. The Financial Conduct Authority in the UK was the first major regulator to act, and others followed.

The core concern is not that prop firms exist. It is that some firms operate in ways that look suspiciously like unlicensed broker-dealer activity. When a firm takes client funds, provides a trading platform, and distributes profits, regulators start asking questions about whether that constitutes regulated financial activity.

Prop firms are not going away. But the unregulated, anything-goes era is ending. The firms that adapt will survive. The ones that do not will get shut down.

Key Regulatory Timeline

The regulatory landscape has moved fast. Here are the major milestones that have shaped prop trading firm regulation news over the past two years.

- Late 2024: FCA issues first public warning about unlicensed prop firms targeting UK traders

- Early 2025: Multiple prop firms voluntarily implement KYC in anticipation of regulatory requirements

- Mid 2025: CFTC and NFA issue joint guidance on disclosure requirements for futures prop firms

- Late 2025: ESMA begins consultation process on retail prop trading classification

- Early 2026: BaFin and AMF independently issue warnings about specific offshore prop firms operating in Germany and France

- 2026 ongoing: Several mid-size prop firms restructure operations to comply with local regulations in key markets

The pace is accelerating. Each regulator that acts makes it easier for the next one to follow. The firms that waited to see what would happen are now scrambling to catch up.

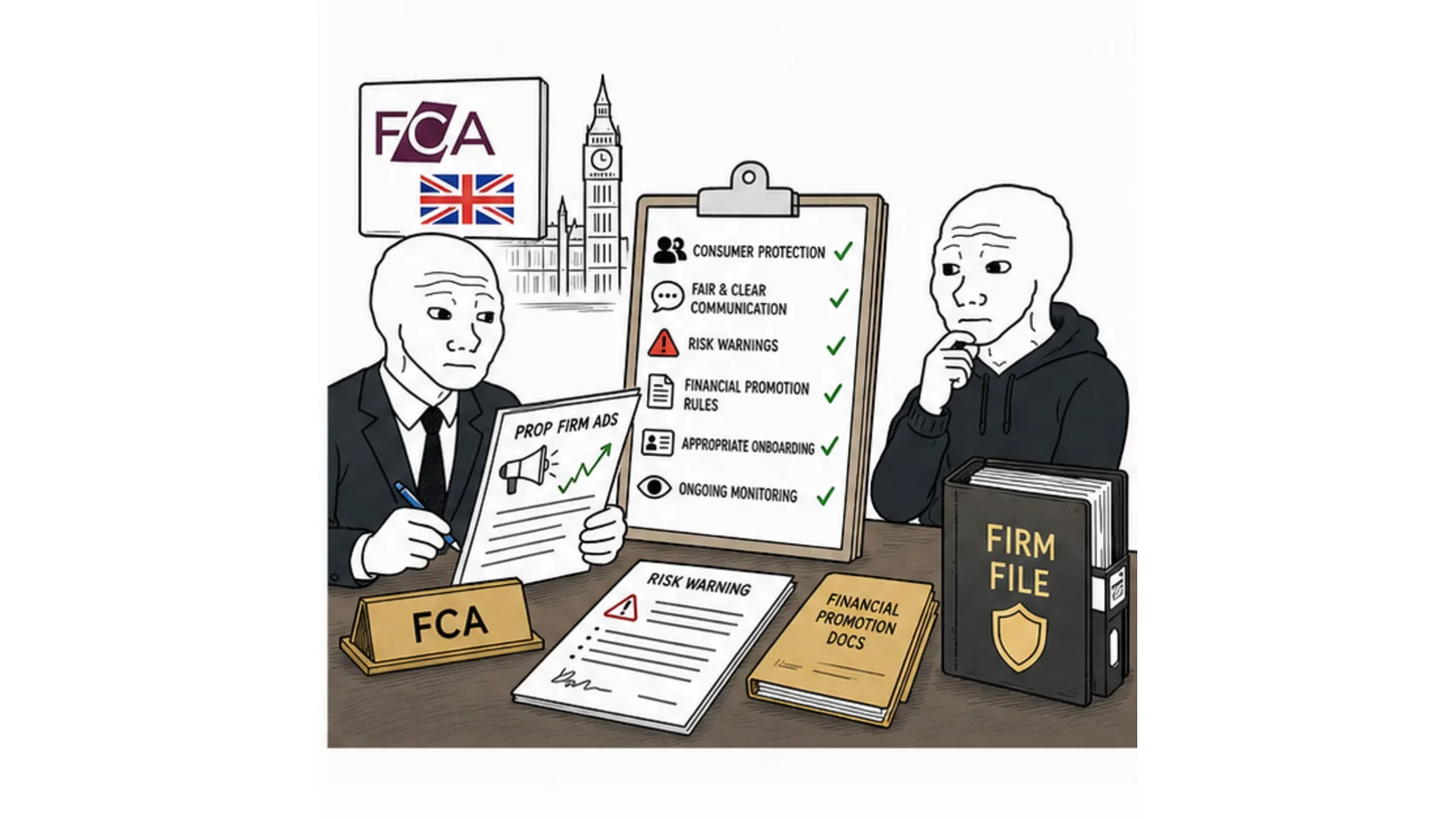

What the FCA Is Doing in the UK

The FCA has been the most aggressive regulator in the prop firm space. In 2024-2025, the FCA issued multiple warnings about prop firms operating without authorization in the UK. Several firms received formal warnings requiring them to either obtain proper licensing or stop serving UK clients.

The FCA's primary concern is consumer protection. They argue that traders paying evaluation fees are effectively consumers, and that prop firms should be subject to the same consumer protection standards as other financial services.

In response, some major prop firms have obtained regulatory licenses or restructured their operations to comply with FCA requirements. Others have simply stopped accepting UK clients rather than go through the licensing process.

For UK-based traders, this means you should check whether your prop firm is FCA-authorized or operates under a valid exemption. If they are not and they are still accepting UK clients, that is a red flag.

The FCA has also signaled that it may pursue enforcement action against firms that continue serving UK traders without authorization. This could include fines, public warnings, and requests to internet service providers to block access to non-compliant firm websites.

CFTC and NFA Actions in the United States

The Commodity Futures Trading Commission and the National Futures Association have taken a different approach. Rather than targeting prop firms directly, they have focused on the relationship between prop firms and their executing brokers.

Futures prop firms in the US are generally easier to regulate because they use regulated futures commission merchants for execution. The CFTC's focus has been on ensuring that prop firms do not mislead traders about the nature of their accounts, particularly around whether traders are using real or simulated money.

The NFA has issued guidance requiring futures prop firms to clearly disclose the difference between demo and live trading environments. This matters because many prop firm challenges use demo accounts during the evaluation phase, and traders have a right to know exactly what environment they are trading in.

US regulation also affects which instruments prop firms can offer. Forex prop firms that serve US traders must use CFTC-registered brokers for execution. Futures prop firms face even tighter constraints, requiring FCM relationships and NFA membership for certain operations. This is why some international prop firms simply exclude US traders entirely rather than navigate the regulatory maze.

For US-based traders, the key takeaway is that futures prop firms face more direct regulatory oversight than forex prop firms, because futures markets are more tightly regulated in general.

The CFTC has also signaled interest in how prop firms advertise their services. Claims about potential earnings, win rates, and account sizes are coming under scrutiny for potential misrepresentation. Firms that make unrealistic income claims may face enforcement action.

ESMA and EU Regulatory Moves

The European Securities and Markets Authority has been slower to act than the FCA but is moving in the same direction. ESMA's concern is that retail traders in EU member states are accessing prop firm services without the protections that EU financial regulations provide.

ESMA has signaled that it may classify certain prop firm activities as regulated financial services, particularly when firms offer profit-sharing arrangements that resemble portfolio management.

Several EU member states, including Germany's BaFin and France's AMF, have independently issued warnings about specific prop firms operating in their jurisdictions without proper authorization.

The EU approach tends to be slower but more comprehensive. When ESMA does finalize its position on prop firms, it will likely apply across all 27 member states simultaneously, which will force major operational changes for any firm serving EU clients.

For EU-based traders, the best approach is the same as everywhere else. Trade with firms that take compliance seriously, keep your own records, and do not put all your trading income into a single firm that could get shut down by a regulatory action at any time.

KYC and AML Requirements Going Mainstream

The most visible regulatory change for traders has been the rollout of KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements across the industry.

Two years ago, most prop firms required nothing more than an email address to open an account. Today, the majority of established firms require identity verification, proof of address, and sometimes source-of-funds documentation.

This KYC verification process is not optional anymore. Firms that skip it are either too small to have attracted regulatory attention yet, or they are deliberately avoiding compliance. Neither is good for you as a trader.

Some traders resist KYC because they value privacy. That is understandable, but it is also unrealistic in 2026. Any firm that handles money, even indirectly, is going to face KYC requirements eventually. No-KYC prop firms exist, but they carry significantly higher risk.

The Financial Action Task Force has updated its guidance to include virtual asset service providers and similar entities, which covers many prop firm payout mechanisms. This means KYC is not just a firm preference anymore, it is an international anti-money-laundering standard.

How Prop Firms Are Responding to Regulation

The prop firm industry is splitting into two camps in response to regulation. Understanding which camp your firm belongs to matters for the long-term safety of your funded account.

The Compliance Camp

Larger, established firms are investing in compliance. They are obtaining licenses, implementing KYC, changing their corporate structures, and in some cases, moving their operations to regulated jurisdictions. These firms cost more to trade with because compliance is expensive. But they are also more likely to be around in five years.

Firms in this camp tend to be transparent about their regulatory status. They publish their license numbers, name their executing brokers, and explain exactly how trader funds are handled. If you ask a firm about their regulation and they give you a clear answer, that is a good sign.

The Relocation Camp

Some firms are responding to regulation by moving their operations to jurisdictions with looser oversight. Saint Vincent and the Grenadines, Seychelles, and the Marshall Islands remain popular registration locations for firms trying to avoid regulatory requirements.

This is not inherently bad, but it does mean you have less recourse if something goes wrong. A firm regulated by the FCA is subject to the Financial Ombudsman Service and the Financial Services Compensation Scheme. A firm registered in St Vincent is not.

The relocation strategy works until it does not. When regulators coordinate internationally, as they increasingly do through bodies like the Financial Action Task Force, offshore registration alone will not be enough to avoid compliance requirements.

The Restructuring Camp

The smartest firms are restructuring their operations so that they genuinely fall outside the scope of financial regulation. This means they do not hold client funds, do not execute trades, and do not provide investment advice. They act purely as evaluation services that test trading skill.

This model is more defensible from a regulatory standpoint, because the firm is not providing a financial service. It is providing a skill test. Whether regulators accept this distinction remains to be seen, but it is the approach most likely to survive long-term.

How Regulation Affects Your Funded Account

Prop trading firm regulation news might seem abstract, but it has real consequences for your funded account. Here is what changes when regulators act.

Payout Methods and Speed

Regulatory pressure has pushed many firms away from crypto payouts toward more traceable methods like bank transfers and Deel. This can mean slower payouts but better documentation for tax purposes.

Account Verification Requirements

KYC requirements mean you will likely need to verify your identity before receiving your first payout. Some firms are retroactively applying KYC to existing funded accounts. If you cannot pass verification, you may lose access to your funded account.

This catches traders off guard regularly. They pass a challenge, request a payout, and then get asked for documents they do not have ready. Get your documents in order before you start trading, not after you have money coming to you. You need a government-issued photo ID, a proof of address dated within the last three months, and sometimes a source-of-funds declaration.

Firm Stability

Regulatory actions have forced some smaller firms to shut down entirely. If your funded account is with a firm that gets hit by regulatory action, your ability to withdraw profits may be affected. Always check a firm's regulatory status before committing significant time or money.

When a firm shuts down due to regulatory pressure, funded traders are often the last to know. The firm stops responding to emails, the dashboard goes offline, and any pending payouts vanish. This is why diversification across multiple firms is not optional anymore. It is basic risk management.

Rule Changes

Firms may change their rules in response to regulatory requirements. This can include modifications to drawdown calculations, news trading restrictions, or position size limits. Always re-read the rules when your firm announces compliance-related updates.

How to Protect Yourself as a Trader

You cannot control what regulators do. But you can control how you position yourself. Here is how to protect your prop trading career from regulatory disruption.

- Only trade with firms that have clear compliance policies, even if they are not formally regulated.

- Complete KYC verification immediately when asked, not after you have a payout pending.

- Withdraw profits regularly rather than letting large balances accumulate in your funded account.

- Diversify across two or three firms so a single regulatory action does not wipe out your entire trading income.

- Keep records of all communications with your prop firm, including payout confirmations and rule change notifications.

- Avoid firms that explicitly advertise their lack of regulation as a feature. That is not a selling point, it is a warning sign.

- Follow prop firm red flag warnings and trust your instincts when something feels off.

Regulation in the prop firm space is not a disaster. It is a cleanup. The industry grew too fast for its own good, and the firms that survive will be the ones that took compliance seriously from the start. The traders who survive will be the ones who did the same. Stay informed, verify your firm's status, and never assume that tomorrow's rules will be the same as today's.