Funded accounts often use simulated or controlled trading environments rather than ordinary brokerage accounts. The NFA BASIC registry is useful when checking any firm or broker claiming US futures-market oversight.

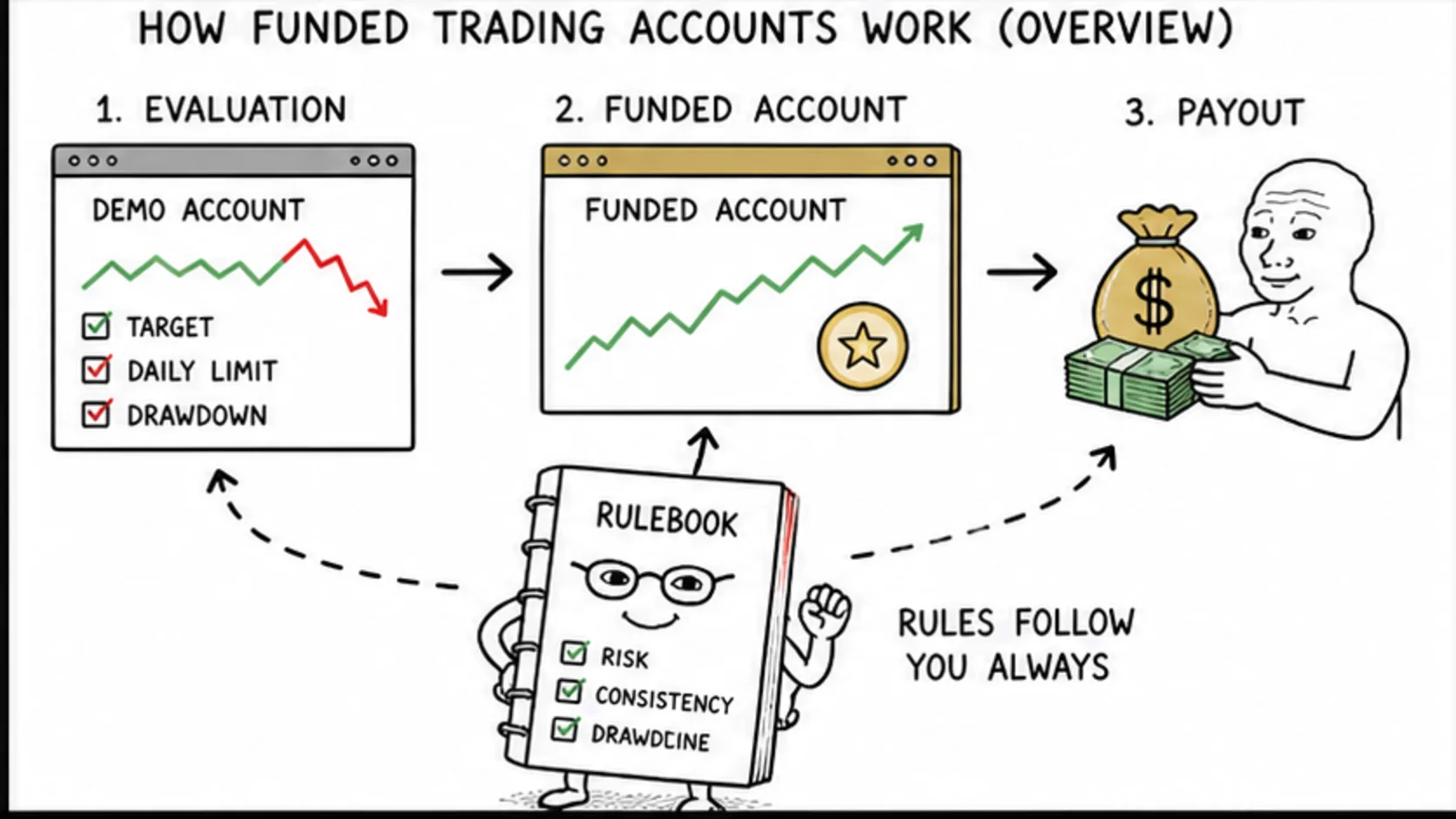

Funded trading accounts work through a simple arrangement. A prop firm gives you capital to trade. You keep a share of the profits. The firm keeps the rest. If you lose money while following the rules, the firm takes the hit. That is the deal.

But understanding the mechanics of how this arrangement actually functions, from evaluation to funded account to payout, is what separates traders who use funded accounts effectively from traders who keep paying evaluation fees and getting nothing back.

Key Takeaways

- Funded trading accounts involve passing an evaluation, receiving capital, and earning profit splits on your trading gains.

- The lifecycle has three stages: evaluation, verification, and funded trading.

- Daily loss limits, maximum drawdown, and consistency rules protect the firm's capital.

- Profit splits of 70-90% are paid every 14-30 days on your cumulative gains.

On This Page

The Deal: How the Arrangement Works

The arrangement between trader and prop firm is built on one core principle. The firm provides the capital, the trader provides the skill, and both sides share the upside.

You pay an evaluation fee upfront. This fee typically ranges from $50 for small accounts to $600 for large ones. The fee covers the cost of administering the evaluation and, candidly, contributes to the firm's revenue from the majority of traders who fail.

If you pass, the firm gives you access to a trading account. Everything you earn above the starting balance is split between you and the firm. The standard split is 80/20 in the trader's favour. Some firms go higher.

If you lose money while following the rules, the firm absorbs the loss. Your personal financial exposure ends at the evaluation fee you already paid. You cannot be charged for trading losses.

The firm protects itself through strict risk parameters. These parameters are not suggestions. They are hard limits built into the platform. Hit them and your trading stops.

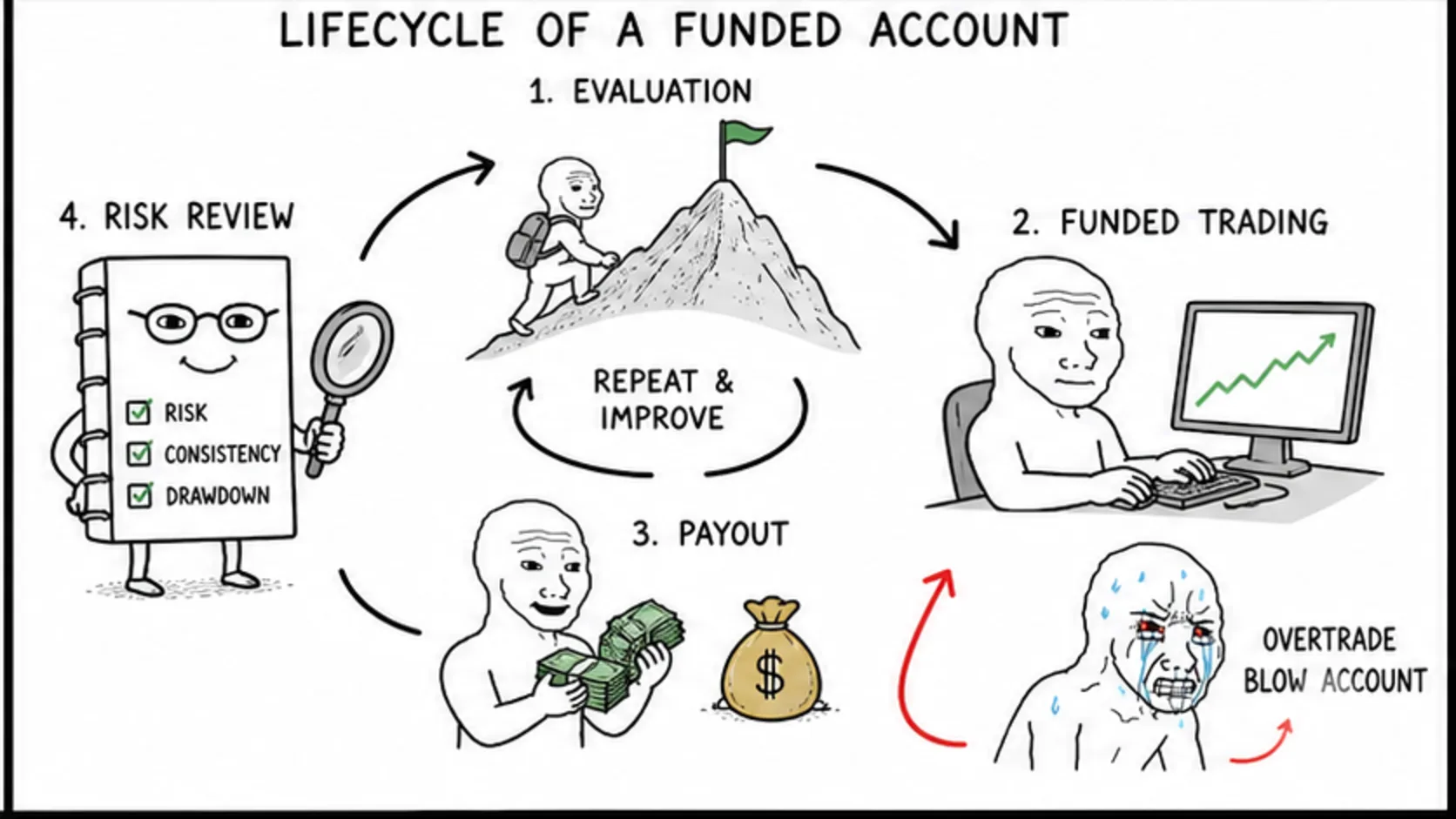

The Lifecycle of a Funded Account

A funded account goes through three distinct stages. Not every firm uses all three, but the structure is common enough that understanding it prepares you for most firms.

Stage one is the evaluation. You prove you can hit a profit target while managing risk. Stage two is verification, a shorter confirmation that your results were not a fluke. Stage three is the funded account itself, where you trade the firm's capital and earn profit splits.

Each stage has its own rules, its own pressure points, and its own failure rate. Let us walk through them.

Phase One: The Evaluation

The evaluation is the gatekeeper. It is where 90% of traders get filtered out, and the filtering mechanism is designed to catch anyone who cannot manage risk under pressure.

You receive a simulated trading account with a specific balance. You have a profit target to hit, typically 8-10% of the account value. On a $100,000 account, that means making $8,000 to $10,000 in gains.

You must hit this target without breaching the daily loss limit, the maximum drawdown, or any other risk parameter. Some firms also require a minimum number of trading days to prevent one lucky trade from passing you.

The evaluation has no partial credit. You either pass all rules simultaneously or you fail. There is no "almost" in prop firm evaluations.

Most firms offer evaluations with no time limit. This is a massive advantage. Take your time. Trade small. Let your edge accumulate slowly. The traders who rush are the ones who fail.

Phase Two: Verification

Not every firm requires verification, but many do. Verification is a shorter evaluation with a smaller profit target designed to confirm you actually know what you are doing.

The verification target might be 5% instead of 10%. The rules are usually the same or slightly more relaxed. The time frame might be shorter.

The point of verification is simple. The firm wants to make sure your evaluation results were not the product of one good trade, one lucky market move, or one desperate all-in that happened to work out.

Think of verification as the firm asking, "Can you do that again?" If you can, you are through to the funded account. If you cannot, you are not ready, and the firm just saved itself from funding an inconsistent trader.

Phase Three: The Funded Account

Once you clear all phases, you receive your funded account. This is where the arrangement becomes real. You trade with the firm's capital under their ongoing rules.

The funded phase rules are typically the same or slightly more relaxed than the evaluation rules. Your daily loss limit and maximum drawdown still apply, but the profit target is gone. You are no longer trying to hit a specific number. You are trying to produce consistent gains over time.

Every dollar you make above the starting balance accrues to your account. On a regular payout schedule, usually every 14 to 30 days, the firm calculates your gains, takes their percentage, and sends you your share.

As long as you stay within the rules and do not breach the risk parameters, the account remains yours to trade. Some firms offer scaling plans that increase your account size based on consistent performance over time.

The Risk Rules That Govern Everything

The risk rules are the architecture of every funded account. They are not guidelines. They are hard limits enforced by the trading platform. Understanding them is non-negotiable.

Daily loss limit. The maximum amount your account can lose in a single trading day. On a $100,000 account with a 5% daily loss limit, that is $5,000. Lose $5,001 and your account closes. No warnings, no grace period.

Maximum drawdown. The maximum distance your account can fall from either the starting balance or the highest balance reached. This can be static or trailing. A trailing drawdown follows your profits upward, which means the floor rises as you make money. This catches many traders off guard.

Consistency rule. Some firms cap how much you can earn in a single day relative to your total profits. If one day accounts for more than 30-40% of your total gains, you may need to keep trading to dilute that day's impact.

Weekend holding rules. Some firms restrict holding positions over the weekend. Others allow it with reduced position size requirements. Know which type you are dealing with.

How Payouts Work

Payouts are the reason you are here. They are also simpler than most people expect.

The firm calculates your gains since the last payout. If your account balance is higher than it was at the start of the payout period, you have a profit. The firm takes their percentage, typically 10-20%, and sends you the rest.

Payout methods vary by firm but commonly include bank transfer, crypto, and Deel. Processing times range from same-day to two weeks depending on the firm.

Some firms require a minimum number of trading days between payouts. This prevents traders from making one trade and immediately withdrawing. Plan for this and build it into your expectations.

Real vs Simulated Accounts

This topic confuses a lot of people. Some funded accounts use real capital in live markets. Others use simulated accounts that mirror live prices exactly but where the firm's actual money is not directly at risk in the market.

In both cases, the trading experience is identical. Your orders fill at market prices. Your P&L moves in real time. Your profit split is real money deposited into your account.

The difference is an accounting one on the firm's side, not a functional one on yours. Whether the account is live or simulated, your job is the same. Follow the rules, produce gains, get paid.

Funded trading accounts work because the firm has engineered a system where risk is bounded on both sides. Your risk is capped at the evaluation fee. Their risk is capped by the daily loss limit and maximum drawdown. Everything inside those boundaries is where trading happens.