Maximum drawdown is the rule version of a regulator warning. The ESMA investor corner repeatedly stresses that retail traders should understand loss exposure before trading.

The maximum drawdown prop firm rule is the line in the sand. Cross it and your challenge is over. Not paused, not warned. Over. The account is closed, the fee is gone, and you start from scratch.

Every other rule works around the maximum drawdown. The daily loss limit prevents you from reaching it in one day. The trailing drawdown is a variation of it. The consistency rule keeps you trading long enough to stay away from it. Maximum drawdown is the brick wall everything else is designed to keep you from hitting.

Here is how maximum drawdown works in prop firms, why recovery gets exponentially harder as drawdown deepens, and how to manage your account so the max drawdown line is something you never see.

Key Takeaways

- Maximum drawdown is the total amount your account equity can fall from its reference point, typically 10-12% of starting balance or highest equity.

- A 50% drawdown requires a 100% gain to recover. The mathematics of recovery are exponential, not linear.

- Maximum drawdown includes unrealised losses from open positions, not just closed trades.

- Static max drawdown stays fixed at the starting balance. Trailing max drawdown follows your highest equity point.

- Keeping your actual drawdown under 5% is the mark of a consistently funded trader.

On This Page

What Is Maximum Drawdown in Prop Firms?

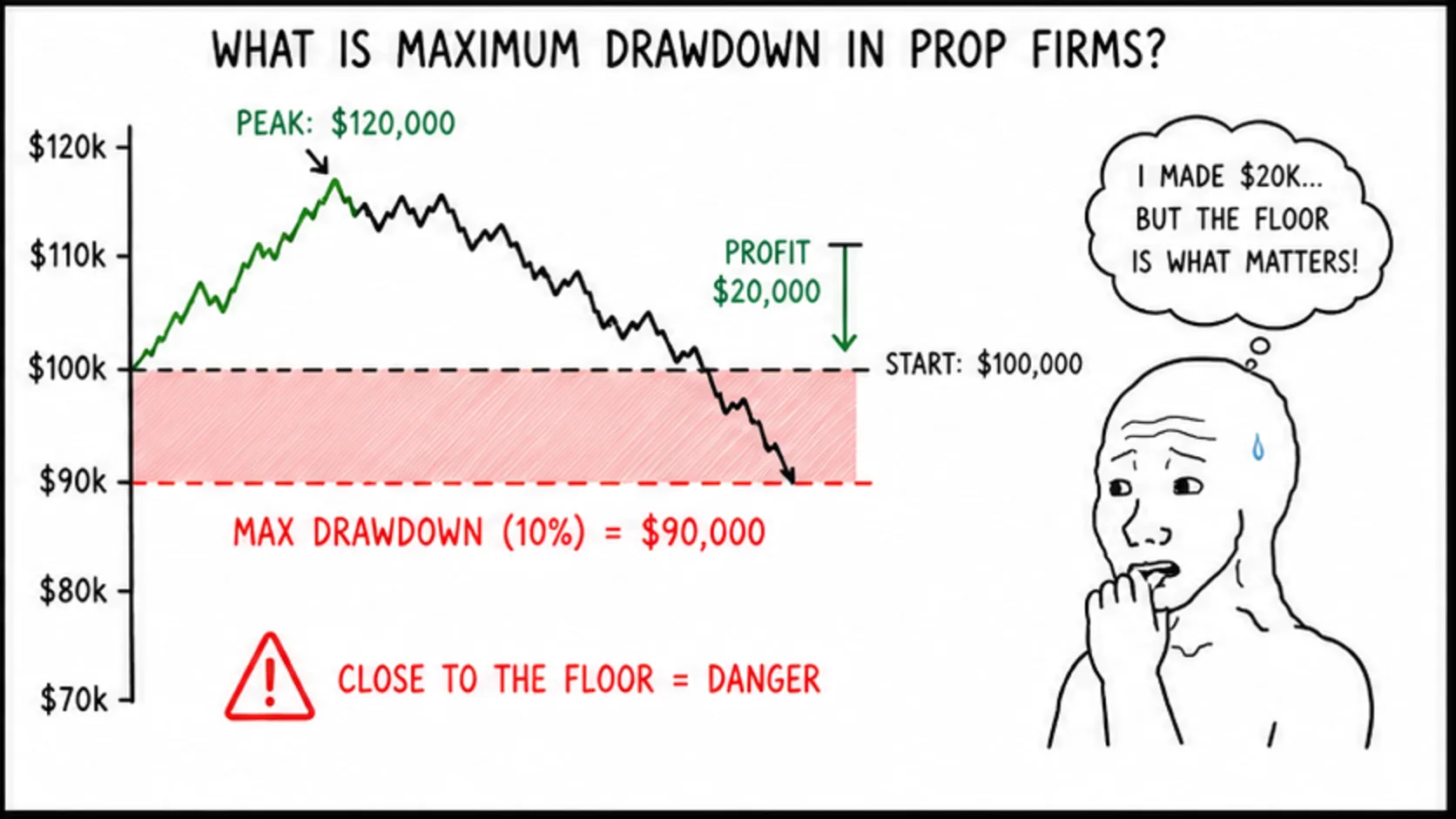

Maximum drawdown is the maximum distance your account equity can fall from its reference point before the firm terminates the account. The reference point is either your starting balance for static drawdown or your highest equity for trailing drawdown.

On a $100,000 account with a 10% maximum drawdown, your equity cannot drop below $90,000. At $89,999, the firm closes everything. The challenge is over.

The practical lesson from funded trading is that you cannot wait until you are near the floor to start caring about the floor. By then, every trade feels like it has to rescue the account, which is exactly when traders start forcing setups.

Most prop firms set maximum drawdown between 8% and 12%. Futures prop firms sometimes go as low as 5-6%. Forex prop firms tend to offer 10-12%.

The higher the percentage, the more room you have, but also the more capital the firm is risking on you.

Maximum drawdown is not a daily rule. It is cumulative. It covers the entire life of the challenge or funded account. Every losing trade, every floating loss, every spread and commission adds to your current drawdown. The meter never resets.

Why a 50% Drawdown Is Devastating: The Math of Recovery

Why is a 50% drawdown harder to recover than a 10% one? Because the math of recovery is not linear. It is exponential. And it punishes you harder the deeper you go.

A 10% drawdown needs an 11.1% gain to recover. A 20% drawdown needs a 25% gain. A 30% drawdown needs a 42.9% gain. A 50% drawdown needs a 100% gain. You have to double your remaining account just to get back to where you started.

This is why prop firms set maximum drawdown at 10-12% and not 30-40%. At 30% drawdown, most traders would never recover. The firm would be funding accounts that are mathematically almost certain to fail.

The average funded trader blows their first funded account within 6 weeks. Not because the market destroyed them. Because they started trading like they owned the place the second they got the green light.

The drawdown creeps up, and by the time they notice, the math is already against them.

This applies to your personal trading too. If you lose 5% of your account, you need a 5.3% gain to recover. Manageable. If you lose 20%, you need 25%. Difficult.

The lesson is simple. Small losses are recoverable. Large losses become mathematically punishing.

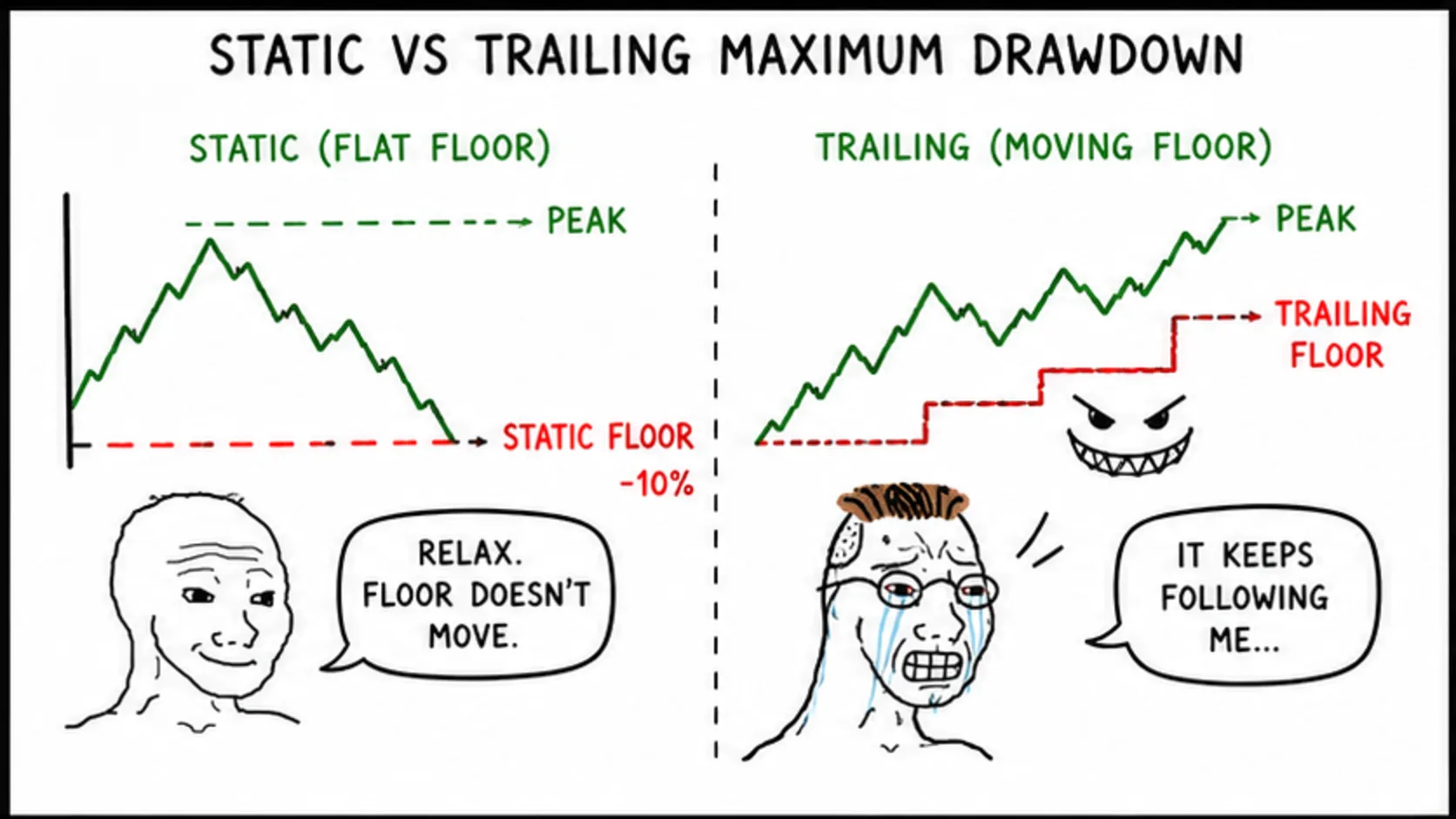

Static vs Trailing Maximum Drawdown

Maximum drawdown comes in two forms. The difference between them is significant.

Static maximum drawdown is measured from your starting balance. On a $100,000 account with 10% static drawdown, your floor is always $90,000.

Whether you grow the account to $120,000 or drop to $95,000, the floor stays at $90,000.

Trailing maximum drawdown is measured from your highest equity point. Same account, same percentage, but your floor moves up as you make money. Grow to $110,000 and your floor becomes $99,000. Grow to $120,000 and your floor is $108,000.

With static drawdown, your safety margin increases as your account grows. With trailing drawdown, your safety margin stays roughly the same in percentage terms but decreases in absolute terms because the floor keeps chasing you. Drawdown timing also varies between EOD and intraday measurement, which changes how much breathing room you have during a session.

If you have the option to choose between static and trailing at your firm, think about your trading style. Consistent daily profits work well with trailing drawdown because the floor moves up gradually. Swing traders with lumpier results are better served by static drawdown.

Floating Losses Count Against Your Max Drawdown

This catches more traders than any other aspect of maximum drawdown.

Your open positions count. If you have $5,000 in floating losses, that $5,000 is counted against your max drawdown even though you have not closed the trades yet.

The firm sees your equity, not just your balance.

You are not stupid. You are just confused. There is a difference. Barely. Traders confuse balance with equity all the time. Your balance only changes when you close trades. Your equity changes in real time. The max drawdown is measured against equity.

This means a single large position can breach your max drawdown even if your closed trade history looks fine. You could have made $3,000 in closed profits but have an open trade losing $8,000.

That puts you $5,000 below your starting balance on a $50,000 account with a 10% max drawdown. Breached.

The fix is to always calculate your current drawdown including floating losses. Before opening any new position, check your equity, not your balance. Know exactly how much room you have.

What Is a Good Maximum Drawdown?

The firm allows 10-12%. That does not mean you should use all of it.

A consistently funded trader keeps their maximum drawdown under 5%. That is the benchmark.

If your equity never drops more than 5% from its peak, you are managing risk properly.

Think of the firm's maximum drawdown as the hard wall. Your personal maximum drawdown should be the soft wall at half that distance. If the firm gives you 10%, your target is 5%. The remaining 5% is emergency buffer for black swan events, spread widening, and unexpected volatility.

What does a 5% maximum drawdown look like in practice? On a $50,000 account, your equity never drops below $47,500 at any point. That means your combined closed and floating losses never exceed $2,500 from your reference point.

If you are sizing your positions correctly, this is achievable. Risking 0.5-1% per trade and keeping total open risk under 3% naturally keeps your max drawdown well within the 5% target.

The 3-5-7 Rule and Maximum Drawdown

What is the 3-5-7 rule in forex? It is a general risk management guideline, not a prop firm rule. Risk 1-3% per trade, keep total open risk at 5% or less, and limit any single market exposure to 7%.

Following the 3-5-7 framework helps you stay within maximum drawdown limits naturally. If you risk 1% per trade and never have more than 5% total open risk, a string of five consecutive losses puts you at 5% drawdown. Manageable. Ten consecutive losses at 1% each puts you at 10%. Uncomfortable but within limits.

The problem is that most traders do not follow any framework at all. They risk 2-3% per trade, have 10% open risk, and then wonder why they breached max drawdown after three losing trades.

The 3-5-7 rule is not magic. It is just structured risk management. Use it or do not, but have some framework in place. Unstructured risk management is not risk management. It is gambling with extra steps.

How to Manage Your Maximum Drawdown

You have three missions for maximum drawdown. Non-negotiable. Always.

Mission one: track your current drawdown in real time. Before every trade, know your equity, your reference point, and how much room you have. Use a drawdown calculator if you need to. This takes 30 seconds and prevents 90% of accidental breaches.

Mission two: reduce position sizes when drawdown exceeds 3%. If your drawdown is growing, do not keep trading the same size. Cut your risk in half. Small positions in drawdown recover faster than large positions. Large positions in drawdown compound losses faster.

Mission three: stop trading when drawdown hits 7%. Not 10%. Not 9%. 7%. If you are more than two-thirds of the way to the max drawdown, close everything and take a day off. The remaining 3% is for market events you cannot control, not for trades you choose to take.

These three rules sound conservative. They are. That is the point. Traders who manage their drawdown conservatively pass challenges. Traders who push their limits become statistics.

The traders who never breach maximum drawdown are not luckier than you. They just respect the math. A 10% drawdown limit is not a suggestion. It is a hard wall. Treat it like one.