Your risk per trade in a prop firm challenge is the single number that determines whether you pass or fail. Not your strategy. Not your win rate. Not your indicators. How much you risk on each individual trade.

The answer is 0.5% to 1% of the account value per position. I am going to show you the exact math behind why this works and why anything higher is gambling with someone else's money.

Key Takeaways

- Risk 0.5-1% per trade during any prop firm evaluation. This gives you 10-20 consecutive losing trades before you breach risk limits.

- 2% risk per trade sounds reasonable in normal trading. In a timed evaluation with a daily loss limit, it is a ticking time bomb.

- 3% risk per trade means one bad day ends your challenge. Two losing trades and you are done.

- Your risk per trade is not the same as your position size. Risk equals account value times risk percentage divided by your stop loss distance.

On This Page

- Why Risk Per Trade Matters More Than Your Strategy

- The Math: Why 0.5-1% Works and 2% Does Not

- How Risk Per Trade Interacts With the Daily Loss Limit

- How Risk Per Trade Interacts With Maximum Drawdown

- How to Calculate Your Position Size From Risk Per Trade

- Real Examples Across Common Account Sizes

- Why 2% Risk Is Too Much for Prop Challenges

- Why 3% Risk Per Trade Is Account Suicide

- Tracking Your Risk During the Challenge

- The Rule That Never Breaks

That risk-first mindset lines up with the warnings from regulators such as the Commodity Futures Trading Commission: leverage magnifies mistakes, so the size of the trade matters as much as the direction.

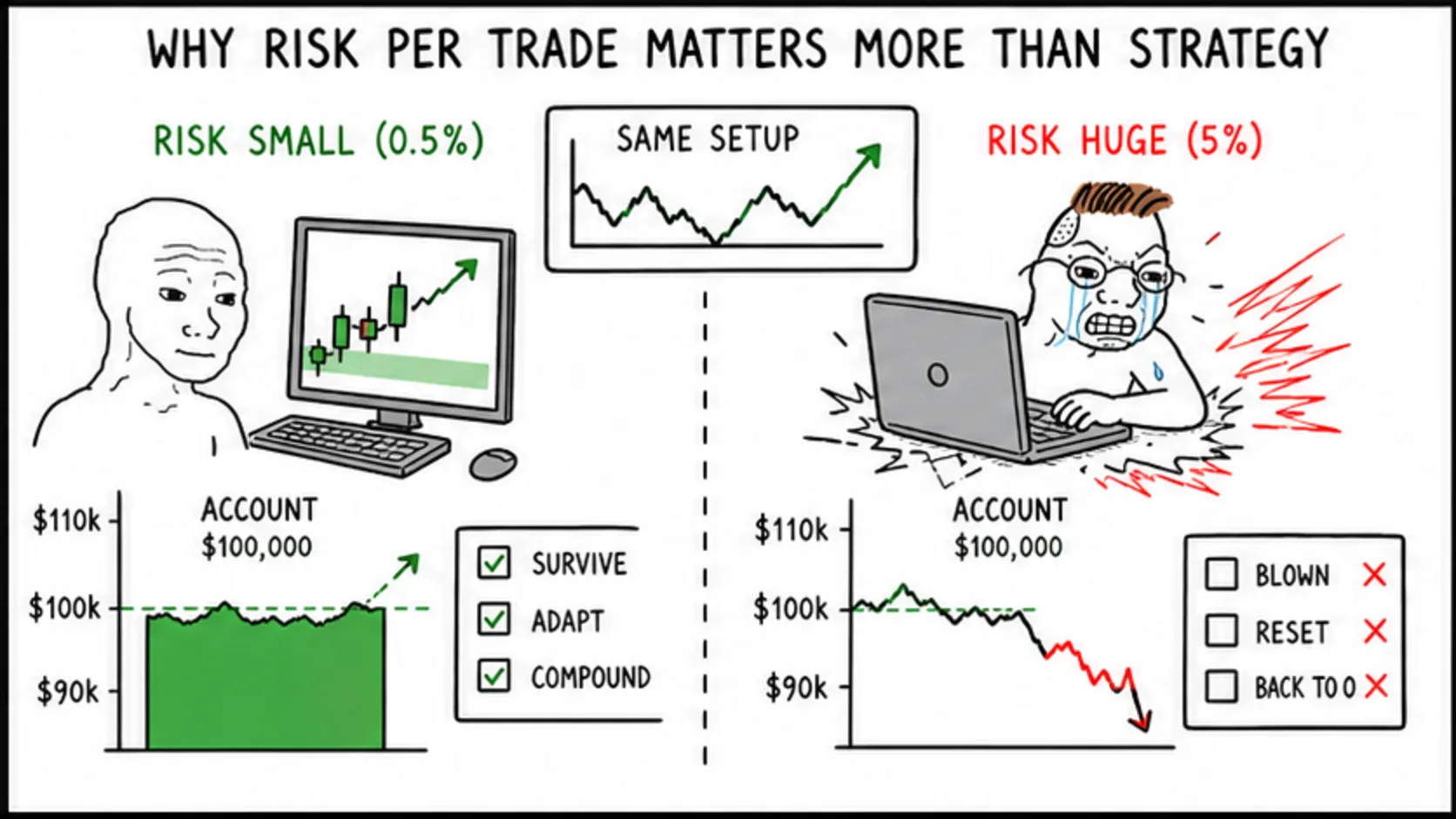

Why Risk Per Trade Matters More Than Your Strategy

Here is the thing nobody wants to hear. A mediocre strategy with 0.5% risk per trade will pass more prop firm challenges than a brilliant strategy with 3% risk per trade.

The prop firm evaluation is not testing your ability to pick winning trades. It is testing your ability to survive long enough to hit the profit target without breaching any rules. Risk management is not optional in prop trading, it is the entire game.

Your risk per trade determines how many shots you get before the rules terminate your account. At 0.5% per trade, you can take 20 consecutive losses on most accounts before you are in danger. At 3%, you get three, maybe four.

Which one gives you a better chance of passing? The answer is obvious. Yet most traders choose the one that gives them fewer chances because it feels more exciting.

The Math: Why 0.5-1% Works and 2% Does Not

Let us run the numbers on a $50,000 account with a 5% daily loss limit and a 10% maximum drawdown. These are standard parameters across most prop firms.

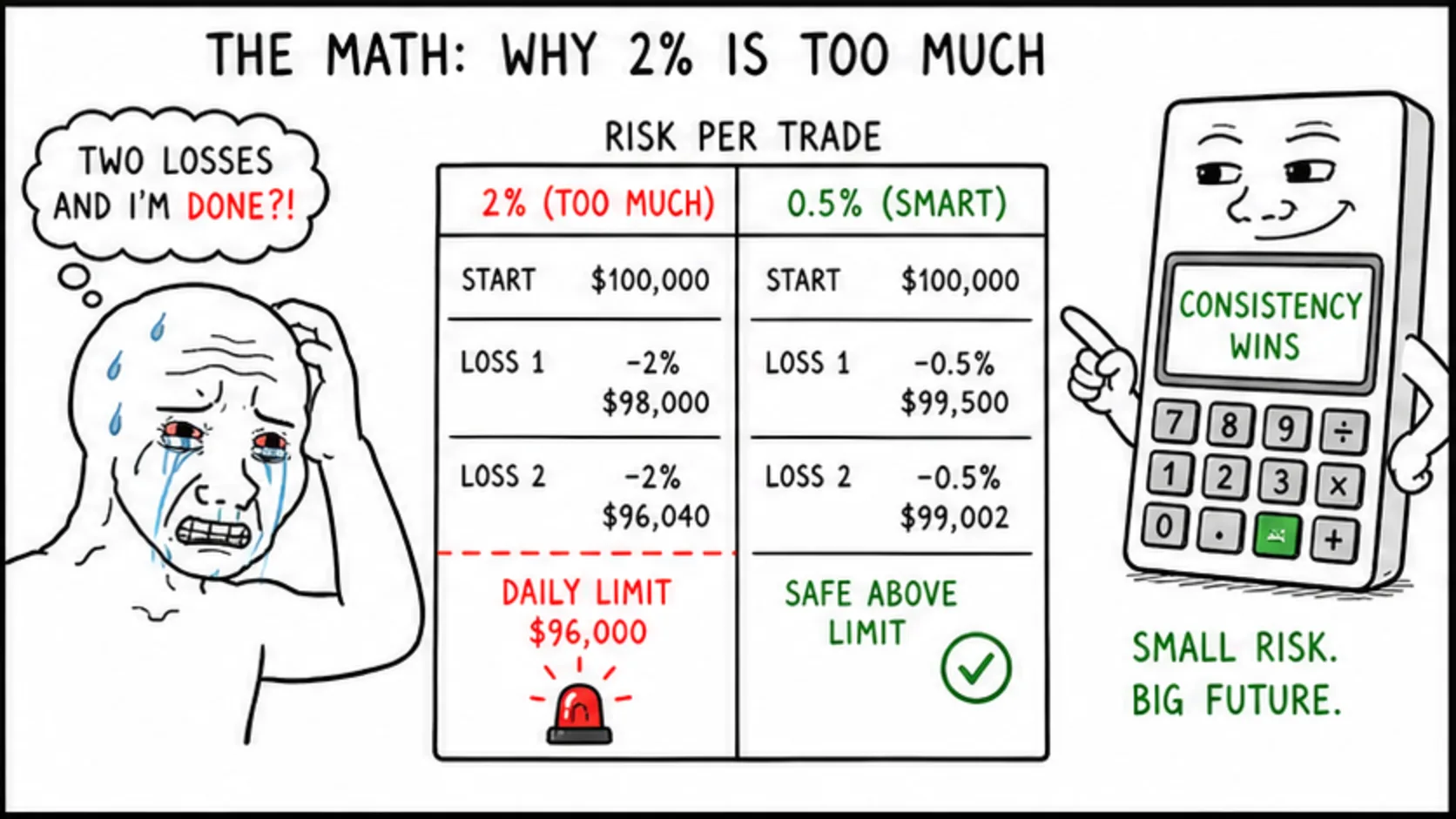

At 0.5% risk per trade, your maximum loss per trade is $250. You can lose 10 trades in a row before you hit your daily loss limit of $2,500. That is ten losses and you are still trading.

At 1% risk per trade, your maximum loss is $500. You can lose 5 trades before the daily loss limit kicks in. Still manageable. Five losses is a bad day, not a blown evaluation.

At 2% risk per trade, your maximum loss is $1,000. You can lose 2 trades before you are done for the day. Two losses and you are sitting on your hands. But here is the real problem.

At 2%, two bad days in a row costs you $4,000, which is 8% of the account. You are now 80% of the way to the maximum drawdown on most challenges. One more bad day and the account closes permanently.

The math is not complicated. Lower risk per trade means more room for error. More room for error means a higher probability of surviving long enough to hit the profit target.

How Risk Per Trade Interacts With the Daily Loss Limit

The daily loss limit is the rule that ends more evaluations than anything else. Your risk per trade determines how close you get to it on a normal trading day.

On a $50,000 account with a 5% daily loss limit ($2,500), here is what different risk levels look like in practice.

0.5% risk ($250 per trade): you can take 10 losses before the daily limit stops you. Even on a terrible day where you take 5 losses and 2 wins, your net loss is around $750-$1,000. Well within limits.

1% risk ($500 per trade): you can take 5 losses before the limit. A normal mixed day of 3 losses and 2 wins might net you a $500-$1,000 loss. Still safe.

2% risk ($1,000 per trade): you can take 2 losses. A single losing trade followed by a revenge trade that also loses puts you at $2,000 down. One more and you are at the limit. No room for a bad streak.

The daily loss limit is not a target. It is a cliff edge. You want to stay as far from the edge as possible. Your risk per trade is how far back from the edge you stand.

How Risk Per Trade Interacts With Maximum Drawdown

The maximum drawdown is the hard floor. Touch it and your account closes. Your risk per trade determines how quickly you approach that floor during losing streaks.

On the same $50,000 account with a 10% maximum drawdown ($5,000 from starting balance), the numbers look like this.

At 0.5% risk, you need 20 consecutive full losses to blow through the drawdown. That is statistically nearly impossible if you have any kind of edge.

At 1% risk, you need 10 consecutive full losses. Also extremely unlikely for a trader with a real strategy.

At 2% risk, you need 5 consecutive full losses. Uncommon but absolutely possible during a volatile week with bad timing. Five losses in a row happens to every trader.

If the drawdown is trailing, the math gets even tighter because every profitable trade raises the floor. Your risk per trade needs to account for the trailing mechanism, not just the static number.

How to Calculate Your Position Size From Risk Per Trade

Risk per trade is not the same as position size. Here is how to calculate the exact position size from your risk percentage.

Step one: determine your risk amount. Account size times risk percentage. On a $50,000 account at 1%, that is $500.

Step two: determine your stop loss distance in pips. If you are trading EUR/USD and your stop is 50 pips away, that is your stop distance.

Step three: determine the pip value for your instrument. For a standard lot on EUR/USD, one pip is worth approximately $10. For a mini lot, $1. For a micro lot, $0.10.

Step four: calculate position size. Risk amount divided by (stop distance times pip value). $500 divided by (50 pips times $10 per pip) = 1.0 standard lot.

That is it. One standard lot with a 50-pip stop on a $50,000 account at 1% risk. Full position sizing breakdown here for every account size.

Real Examples Across Common Account Sizes

Here are the exact numbers for the most common prop firm account sizes at 0.5% and 1% risk per trade.

$10,000 account. 0.5% risk = $50 per trade. 1% risk = $100 per trade. Daily loss limit at 5% = $500. At 0.5% risk, you get 10 trades before the daily limit.

$25,000 account. 0.5% risk = $125 per trade. 1% risk = $250 per trade. Daily loss limit at 5% = $1,250. At 1% risk, you get 5 trades before the limit.

$50,000 account. 0.5% risk = $250 per trade. 1% risk = $500 per trade. Daily loss limit at 5% = $2,500. At 1% risk, you get 5 trades before the limit.

$100,000 account. 0.5% risk = $500 per trade. 1% risk = $1,000 per trade. Daily loss limit at 5% = $5,000. At 1% risk, you get 5 trades before the limit.

The pattern is consistent. At 1% risk, you get approximately 5 full-loss trades before the daily limit on any account size. At 0.5%, you get 10. More room, more chances, higher probability of passing.

Why 2% Risk Is Too Much for Prop Challenges

People ask this constantly. "Can you risk 2% per trade on FTMO?" Technically, yes. FTMO and most other firms do not enforce a per-trade risk limit. They only enforce the daily loss limit and maximum drawdown.

But just because you can does not mean you should. Here is what 2% risk looks like in practice on a $100,000 account.

2% of $100,000 is $2,000 per trade. The daily loss limit at 5% is $5,000. You can take 2 full losses and you are at $4,000 down. One more loss and you breach the daily limit and your evaluation ends.

Two losses. That is all the room you have at 2% risk. Two trades where your stop gets hit and you are done for the day, possibly the challenge.

The 2% rule comes from personal trading advice where you trade your own money with no daily loss limit and no time pressure. In a prop firm evaluation with both of those constraints, 2% is reckless.

Why 3% Risk Per Trade Is Account Suicide

If 2% is too much, 3% is certifiable. Let me show you exactly why.

3% of a $50,000 account is $1,500 per trade. The daily loss limit is $2,500. One full loss puts you at $1,500 down. Two losses puts you at $3,000, which breaches the daily limit.

You cannot even afford two losing trades in a single day at 3% risk. One bad trade and a revenge trade and your challenge is over.

Over multiple days, three losses at 3% each is $4,500, which is 90% of the way to the maximum drawdown on a 10% drawdown account. One more loss and the account closes permanently.

Anyone recommending 3% risk per trade for a prop firm evaluation has either never taken one or is trying to sell you a reset.

Tracking Your Risk During the Challenge

Knowing your risk per trade is pointless if you do not track it. Here is the system.

Before each trade, calculate your exact risk. Account balance times risk percentage. Then calculate your position size from that risk amount and your stop distance.

After each trade, log it. Entry price, stop loss, position size, actual risk taken. If you took more risk than planned, write that down too.

At the end of each day, check your total risk exposure. How much did you risk across all trades? How much did you actually lose? Where are you relative to the daily loss limit and maximum drawdown?

The traders who pass evaluations are the ones who know these numbers at all times. The ones who fail are the ones who estimate and hope.

The Rule That Never Breaks

0.5-1% risk per trade. No exceptions. Not on your best setup. Not on your worst day. Not when you are $500 from the target. Not when you are frustrated after three losses.

This rule is boring. It is unsexy. It is the opposite of what the YouTube traders with rented Lamborghinis will tell you.

But it is the rule that separates funded traders from the 90% who keep buying evaluations and wondering why nothing works.

Your risk per trade is your survival mechanism. Treat it that way. The market will test you. The rules will pressure you. Your emotions will try to convince you that this one time, just this once, it is okay to size up.

It is never okay. Not once. Not ever. The account does not care about your reasons. It only cares about the numbers.